STOCK MARKET BEHAVIOR THAT WE LEARN FROM THE 100-YEAR MARKET MOVEMENTS

1. There seem to be consecutive "patterns" of Good and Bad results for the Dow in roughly 20-year periods.

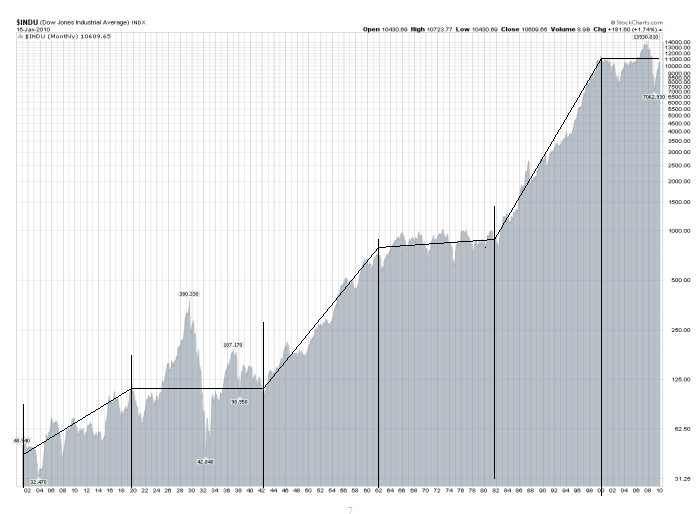

- 1900-1920 GOOD Constant growth (1920 Dow price

2.5 times 1900 Dow price)

- 1920-1940 BAD Worst decline in history (-90%);

1940 price about the same as 1920

price

- 1940-1960 GOOD Sustained growth (1960 Dow 4.7

times 1940 Dow)

- 1960-1980 BAD 1% annual growth average over 20

years, with 5 "crashes" of 25-45%**

- 1980-2000 GOOD Best 20-year history, everybody made

money

- 2000-2010 BAD Disaster - Two huge crashes (-45% in

2000-02 and -55% in 2008-09)

- 2010-2020 GOOD No real big crashes; up +240%

in the decade.

1960-1980

** If you can't see the 5 crashes in 1960-80, its because a

logarithmic scale makes it hard to see. In the 1970's the

Dow dropped by 45%.

https://mipstiming.com/100_year_dow__1960_1980_

BTW - The Dow grew by 22% in this 20-year period (that's

1%/year) and the the price of the average house in the US

went up by 60%. Bond interest rates averaged about 5%

during this time period, so your bond assets would have

grown by a total of 165% in this 20-year period.

BAD periods almost always follow high-growth, overbought, GOOD periods, as the market "corrects" itself to the long-term trend line (reverts to the mean). What this says is that there were some 20-year periods in the stock market when you just couldn't help but make money, and there were other 20-year periods when it was almost impossible to make money in the market by being long (like in 1960-80 and in 2000-10). This is where the benefits of short selling become apparent.

2. What do the Good/Bad periods above tell us ?

- In order to make good decisions when buying or holding any type of "investment" (stocks, bonds, real estate, gold, etc.), one needs to know what the investment "climate" of market indicators and trends is like at the time. It is obvious from the discussion in #1 above that, in a Good Period like 1980-2000, it would have been difficult for any decision to result in really bad, lasting financial damage. Even if you did make a mistake, the stock market would have made it OK for you in a few years at the latest. For example, if you had bought at the top of 1987 right before a 37% correction, you would have been even in about 3 years and would have gone on to make 4 times your money by the end of this 20-year period. On the other hand, if an investor had made a bad decision in a Bad Period like 1929-1940 or 1960-1980, it could have been a life-changing mistake. For example, if they had bought at the top in 1929, it would have been 26 years (1955) before the price of the Dow would have recovered to the price when they bought it. In this timeframe, they could have made about 4 times the value of their initial investment had they simply invested in mid-term bonds. Of course, had they been in "short" positions during this time period, they could have made 5-10 times their initial investment.

- When considering the above, please realize that 20-30 years usually constitutes an individual's entire investment lifetime. For example, most people are busy paying bills, buying automobiles, buying homes, etc., until they are 35-40 years old. So, many of them really may not have put away much in savings until that time. And, no one wants to invest all of their savings, so they start investing only after they have excess money above the level of saving that they feel comfortable with. By the time age 65 comes along, the bulk of people that have enough to retire do so (and then they are taking money out monthly, not putting more in). Therefore the bulk of most people's investment lifetime is the 20-30 years between ages 35/40 to 60/65.

3. The Dow has had an average compound growth rate of about 7% over the last 110 years.

Recent Examples:

- 1980-2000 Avg Compound Growth = +14.6% GOOD

- 2000-2010 Ave Compound Growth = - 1.6% BAD

- 2000-2010 Ave Compound Growth = +10% GOOD

<<< Compound Growth Calc.- http://www.investopedia.com/calculator/CAGR.aspx >>>

4. If we could avoid the bulk of the large stock market drops, we would do much better than a 10% per year average compounding rate.

- The 4 worst market drops in the last 110 years occurred in

1929-32; 1973-74; 2000-03; and in 2007-09.

- The first two "corrections" above had "double dip" drops

(that is, they dropped 30-50% from their tops; recovered

about ½ of this 1st drop; and then resumed a 2nd leg down

before the correction ended.

- In 2007-10, the 1st leg down was 50%; and the "recovery"

has recaptured about 2/3 of this first drop (just like the

previous two above). So, is this correction going to play

out like the others before it with a 2nd leg down, or is it going

back up to its top from 2007, or is it just going to go sideways

for many years like in Japan? I am relying 100% on MIPS

market trends timing system to answer that for me when the

time comes.

5. Use MIPS stock market timing systems for warning of downdrafts.

- Over time, we "dampened" MIPS to basically ignore very short-term price movements in the market's direction and programmed it to wait until there were signals of "major" changes in the direction of the market, looking for stock/ETF trends. This has helped MIPS decide when to get us out of the market and when to get back in. We will miss the early parts of some major changes, but we will greatly reduce our chance of being whipsawed. Identifying these stock market indicaors and trends will allow us to avoid a large percentage of the market "downdrafts" and get us back in the market in time to make money in the "recoveries".

6. Lower your risk with the asset allocation that is best for you.

- Obviously, you can lower your risk in the stock market by adjusting the percent of your total investment money that you have in equities. Your total assets are made up of real estate, art, personal property, gold, and investment assets. For this analysis, your "investment money" includes: (a) Fixed Income (cash, bonds, and/or bond funds), and (b) Equities (stock and/or stock funds).

Some financial advisors recommend that the % of your investment money that you have in bonds should equal your age (i.e., 40% at age 40; 60% at age 60, etc.) and, of course, the remainder should be in equities. In all discussion herein, remember we are always talking about the stock portion of your investment money. The rest should be in cash, bonds, etc. And it never includes what you should have invested in other assets, like real estate, etc.

Here is what the pros say about the market performance with various asset allocations:

· RISKY PORTFOLIO - 80% stocks, 20% bonds

Throughout history, this portfolio has averaged 10.0% a year.

Its WORST year was a loss of 34.9%.

It lost money 28% of the years.

· BALANCED PORTFOLIO - 60% stocks, 40% bonds

Throughout history, this portfolio has averaged 8.7% a year.

Its WORST year was a loss of 22.5%.

It lost money 22% of the years.

· SAFE PORTFOLIO - 40% stocks, 60% bonds

Throughout history, this portfolio has averaged 7.0% a year.

Its WORST year was a loss of 10.1%.

It lost money 18% of the years.

7. Manage all (or some) of the "Stocks" portion of your portfolio in Section #6 above with MIPS